The ETF Market: Preparing for a New Horizon

The ETF Market: Preparing for a New Horizon

Exchange-traded funds have evolved significantly since their debut in the early 1990s. Most of the growth in the multitrillion-dollar market has been fueled by passive products, but actively managed ETFs may have an impact on the next wave.

On Monday, April 20, a NYMEX oil futures contract traded in negative territory for the first time ever as lackluster demand and scarce storage in the face of the coronavirus pandemic meant that sellers effectively were paying buyers to take a barrel of West Texas Intermediate crude off their hands. Although this event happened just one day before the futures contract expired, the effect on broader oil stocks was limited; institutional players had mostly rolled their futures positions to the next month’s expiration. But the implications of this event went well beyond the niche world of physical-delivery oil futures — it had a profound impact on the exchange-traded products that are based on these futures contracts. The United States Oil Fund, an exchange-traded fund (ETF) that invests primarily in light, sweet crude oil futures, fell 25 percent the next day.

Launched in the U.S. in 1993, ETFs have changed the face of investing over the past two decades. Offering a diverse array of investments at a low cost, these open-ended, index-based funds started out as transparent, liquid, efficient and simple instruments that trade on an exchange like stocks: Borrowing shares to sell short, placing limit or stop-loss orders and buying on margin are all permissible. Although ETFs have some similarities with mutual funds — both represent professionally managed baskets of securities — ETFs are characterized by higher liquidity and greater flexibility because they can be bought and sold over the course of a day. Because typical ETFs are less actively managed than mutual funds, they tend to have lower management fees.1 Moreover, when an investor wants to buy shares of a mutual fund, the process requires an understanding of loads and redemption fees.

ETFs have had a material effect on the way investors access markets. The funds appeal to long-term investors, who use them for index investing, as well as more-active traders with short-term horizons.2 Compared with mutual funds, ETFs are generally more transparent and tax efficient. Portfolio holdings are disclosed daily, in contrast to mutual funds, which report them quarterly with a month’s lag. Most ETFs are passive index funds with very low turnover — and hence few realized capital gains. When there are gains, they are rarely distributed due to ETFs’ distinctive creation and redemption mechanism.

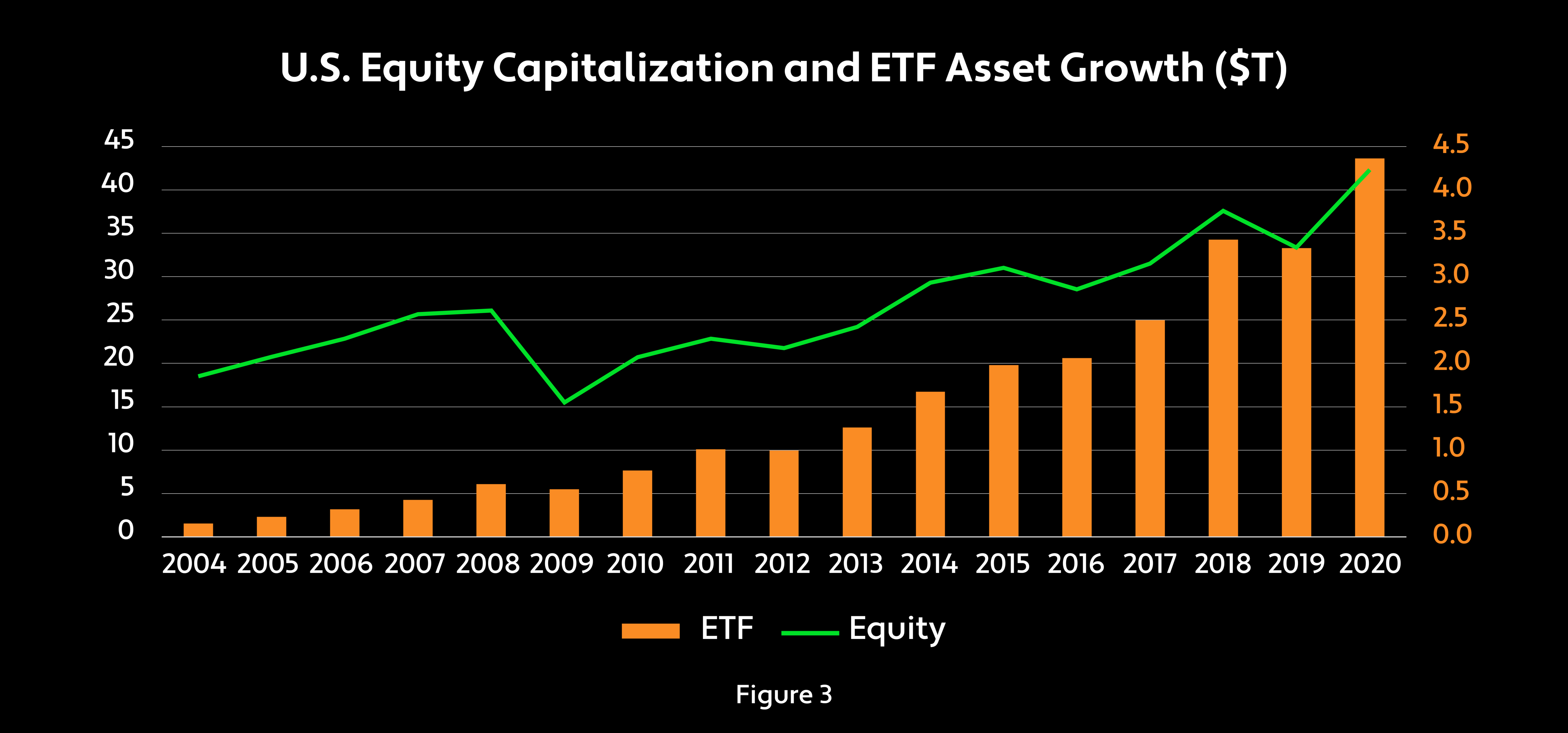

The ETF growth story is best captured by looking at both the number of funds in the marketplace and the value of their assets. Figures 1 and 2 show a linearly increasing number of ETFs accompanied by a nonlinear increase in assets. The nonlinear asset growth can be attributed to the popularity of the most liquid ETFs, which have garnered substantial inflows.3 The funds’ liquidity, based on average daily dollar volume traded, has also grown significantly over the past decade, after a slight lull in the wake of the 2008–’09 global financial crisis. Starting from about $100 billion in assets in 2000, the global ETF industry had grown to $6.35 trillion by the start of this year and is anticipated to reach $10 trillion in the next three years.4

Exchange-traded products have evolved substantially from the simple structures of the first generation. These passive products typically held baskets of stocks or other securities reflecting the composition of the index they were designed to track. Subsequent generations of ETFs were able to replicate the index’s performance by holding a subset of stocks or using swaps or other derivatives. But the rapid growth of the ETF market and the increased variety and complexity of exchange-traded products, including those that incorporate active management strategies or use leverage, have introduced a whole new set of risk factors. The industry’s future growth is likely to depend on the willingness of investors to accept the added risks and increased complexity of the products, and to embrace the active pursuits of ETF providers.

First-Generation ETFs

Exchange-traded funds are the brainchild of the late Nathan (Nate) Most, a self-described “commodities man” who came up with the novel idea in the 1980s while heading new product development at the American Stock Exchange.5,6 At the time, investors who wanted access to the S&P 500 index had to use open-ended mutual funds, which are bought and sold at net asset value (NAV) and priced only once a day, after the close of trading, following rules dating back to the Investment Company Act of 1940, known as the 1940 Act.

Most saw a market for an index fund that could be traded throughout the day and used his experience in the commodities industry to develop a mechanism to allow it. The solution was what he called a “creation unit” — essentially, a large basket of stocks that institutions can exchange for shares in the fund, similar to the receipts that a warehouse issues to owners of commodities stored there. ETFs are relatively inexpensive to run because only authorized participants (APs) — typically, large financial institutions — can create or redeem shares. As ETF shares are in-kind transaction products, no cash is needed to buy or sell them to the fund; because no taxable income is generated during the creation–redemption process (shares are exchanged for the basket of underlying securities), ETFs are more tax efficient than mutual funds.

It took three years for Most to sell AMEX management on his idea and another three years for the Securities and Exchange Commission (SEC) to grant ETFs an exemption from the 1940 Act. In January 1993, AMEX launched the SPDR S&P 500 ETF Trust (SPY) — known as “Spider” for short — managed by State Street Global Advisors. Within a few years, other ETFs had appeared.

The first generation of ETFs were plain-vanilla indexing strategies that tracked the returns of a specific market index by holding all the securities in the index. But they weren’t without risk. ETF managers are required to actively rebalance their portfolios regardless of the volatility or liquidity of the market, making it almost impossible for them to track their benchmarks perfectly.7 To reduce a fund’s tracking error, an ETF manager may lend the underlying securities to hedge funds and other market participants looking to sell the stocks short, creating risk for the ETF investors if the counterparties were to default. First-generation ETFs often used index-linked notes and other derivatives for cash management activities like dividend payments, creating additional counterparty risk.

Exchange-traded products gained popularity because they targeted both institutional and retail demand for diversification coupled with lower investment and operating costs than traditional index mutual funds, which in the early 1990s had annual management fees as high as 2 percent.7 Institutional investors embraced ETFs because of the added advantage of easy settlement (compared with swaps), intraday trading capacity and reduced counterparty risk (again, compared with swaps). Retail investors flocked to these products thanks to their lower costs and the ease of trading them through online brokerage platforms.8

Second-Generation ETFs

The mechanism used by first-generation ETFs worked well for large, liquid benchmarks like the S&P 500, but it was difficult to implement for indices whose underlying stocks were less liquid or more expensive to trade. As a result, by the mid-’90s, second-generation ETFs eased the requirement to hold the whole array of an index’s securities and instead focused on owning a representative selection that tracked as closely as possible the index’s returns. These ETFs typically use quantitative methods to determine the optimal portfolio to replicate an index’s performance and will often hold the securities that have the largest weights in the benchmark.9 This generation of ETFs targets low tracking error and low transaction costs.10

Second-generation ETFs provided access to international equity markets and to very broad, diversified indices tracking entire economies. In 1996, iShares debuted international ETFs in the U.S., including 17 different country funds spanning the globe from Canada to Japan.

Bond ETFs also developed under this paradigm, but for fixed income ETFs, the replication is a much less exact science. The ETF manager is unlikely to be able to access every bond in the underlying index. Instead, it creates a portfolio of bonds designed to track the duration, quality, maturity and exposure characteristics of the index within reasonably tight bounds. Some bond ETFs were constructed using short positions in various interest rate swaps hedged by long positions in high-yield bonds.

Like their first-generation cousins, second-generation ETFs can experience counterparty credit risk if their managers engage in securities lending or use derivatives for cash management.11 And although second-generation ETFs attempt to closely mimic the performance of the target index, they are not immune to tracking error risk.

Third-Generation ETFs

ETFs that track the S&P 500 are naturally capitalization weighted and have Fama–French factor loadings (which show the relationship of different variables to the underlying Fama-French factors). Funds with different weighting schemes — equal weighted, revenue weighted, dividend weighted — started to appear on the landscape in the early 2000s. Their performance, risk and volatility profiles are different from cap-weighted ETFs because the varied weighting schemes are exposed to different factors, depending on their construction. Equal weighting, for example, will typically shift an ETF toward smaller companies, while dividend weighting will generally tilt it toward value stocks.

As the ETF industry developed, providers introduced many new products that were far from plain vanilla. These exchange-traded products (ETPs) employ a variety of different structures, including exchange-traded derivative contracts (ETDCs), exchange-traded commodities (ETCs) and ETNs. ETDCs are standardized derivatives contracts that trade on an exchange; many exotic ETF products use this structure. ETCs track the performance of commodities markets. Barclays Bank introduced ETNs in 2006 to allow retail investors to invest in commodities, currencies and other hard-to-access markets. They are senior, unsecured, unsubordinated debt securities issued by a bank and listed on an exchange, and they can be either collateralized or uncollateralized. Credit risk is partially hedged for collateralized ETNs, but uncollateralized ETNs are fully exposed to counterparty risk.

These third-generation ETFs have one thing in common: They employ swaps or other derivatives to replicate the performance of an index rather than investing in its underlying securities. The manager of these synthetic ETFs typically replicates the index’s performance by entering into a swap contract with a financial institution, often a bank. The swap counterparty agrees to pay the index return, including dividends, to the ETF in exchange for a swap fee and the return on a basket of securities held by the ETF as collateral. The collateral securities do not have to be the same as the securities in the index (in fact, they often are not). This structure is known as an unfunded swap (Figure 4).

Synthetic ETFs can also be created using funded swaps. In a funded swap, the counterparty deposits the collateral securities with an independent trustee to hold on the ETF’s behalf. The collateral in that account is pledged to the ETF and is technically its property. The funded swap structure came into vogue in the wake of the global financial crisis to protect ETFs from the risk of their counterparties going bankrupt.

Proponents of synthetic ETFs claim the funds do a better job of tracking an index’s performance than first- and second-generation ETFs and provide a competitive offering for investors seeking access to remote-reach markets, less liquid benchmarks or difficult-to-execute strategies that would be costly for traditional ETFs to operate.12

Critics of synthetic funds point to several potential dangers, including counterparty risk, collateral risk, liquidity risk and conflicts of interest. A 2018 report on exchange-traded funds by the European Central Bank found that “while counterparties are typically connected with many ETFs, most ETFs rely on a single counterparty.”13 In many cases, counterparties are connected to ETF issuers through ownership links to the same parent bank. In addition, investors may not be aware of the complexity of the relationships between ETFs and their counterparties.14

Fourth-Generation ETFs

The first three generations of ETFs are passively managed, tracking both large indices and those that are less well known. In March 2008, Bear Stearns launched the first actively managed ETF — a current yield fund called Triple-Y that aimed to generate higher returns than a money market fund by investing in a diversified basket of fixed income securities.15 The fund was rebranded under the J.P. Morgan moniker after the bank acquired struggling Bear Stearns that same month, on the eve of the 2008–’09 financial crisis.

Today there are nearly 400 actively managed ETFs in the U.S., representing approximately $125 billion in assets.16 PIMCO’s Enhanced Short Maturity Active Exchange-Traded Fund (MINT), with nearly $14 billion in assets, is the largest actively managed ETF, mainly holding corporate debt with less than one year in remaining maturity. Similarly, the $13 billion JPMorgan Ultra-Short Income ETF (JPST) seeks to maintain a duration of one year or less by investing in investment grade, U.S. dollar–denominated fixed, variable and floating-rate debt. Such active bond ETFs appeal to investors seeking relative safety but higher yields than those offered by money market instruments or long-term Treasury securities. Until recently, actively managed ETFs were largely restricted to such niche segments.17

Most actively managed ETFs are as transparent as traditional ETFs: They publish online a full list of their holdings on a daily basis. That transparency, however, can reveal a manager’s strategy and create the risk of arbitrage by other investors trying to front-run its positions. To combat that, some ETF providers have gotten the SEC to loosen the regulations and approve several actively managed, nontransparent exchange-traded funds (ANTs). These new actively managed ETFs disclose their holdings monthly or quarterly, or share a proxy for their holdings; they are not required to disclose them on a daily basis. In the spring of 2020, American Century launched the first actively managed nontransparent ETFs: the American Century Focused Dynamic Growth ETF (FDG) and the American Century Focused Large Cap Value ETF (FLV).18

The appeal of actively managed ETFs is that they trade like a stock but are structured like a mutual fund. While passively managed ETFs are designed to replicate an index, actively managed ETFs aim to outperform a benchmark return. To put it differently, passively managed ETFs offer the same exposure as the market, known as beta, while actively managed ETFs focus on generating higher returns than a benchmark, known as alpha. Not surprisingly, actively managed ETFs typically have higher costs than their passive counterparts.

The Future Evolution of ETFs

In the U.S., ETFs and mutual funds come under the purview of the 1940 Act. Going back to the era of Nate Most, ETFs have needed to obtain exemptions from certain stipulations in the law that require mutual funds to be purchased and sold only at net asset value at the end of the business day. Since 1993, however, the SEC has issued more than 300 exemptive orders for ETFs, allowing them to be traded throughout the day on secondary markets like the New York Stock Exchange (NYSE).

When ETFs redeem shares through authorized participants, they provide the basket of underlying securities in kind, without selling in the open market and redeeming in cash. There is further tax efficiency because the ETFs can choose to redeem securities that have a lower cost basis, increasing the average cost basis of the shares held by the ETF and thus reducing future capital gains.

When the basket of securities used in the creation or redemption process is in the same proportion as the overall ETF portfolio, it is called a “pro rata slice” basket. Older ETF firms have had the ability to create and redeem shares using non–pro rata slice, or “custom,” baskets, which don’t exactly match the full ETF portfolio in composition. This has several benefits for the ETF provider, including improved fund efficiency and reduced internal trading costs, as well as increased efficiency for APs, leading to tighter spreads. Younger ETF firms, however, did not have this flexibility, creating an uneven competitive landscape with their older rivals.19

On September 26, 2019, the SEC approved a new rule designed to modernize ETF regulation “by establishing a clear and consistent framework for the vast majority of ETFs.”20 The rule allows open-end ETFs to operate without obtaining an exemption from the 1940 Act as long as they provide daily portfolio transparency on their websites. ETFs are permitted to use custom baskets of securities that “do not reflect a pro-rata representation of the fund’s portfolio” or do not exactly match the full ETF portfolio in composition. The website disclosure is intended to inform investors about the cost of investing in an ETF and the efficiency of its arbitrage process. According to the SEC, the new rule is meant “to level the playing field” by allowing all ETFs that rely on it to create and redeem shares using custom baskets, as well as to “protect ETF investors.”21

The SEC has also approved various systems that can be used to introduce actively managed ETFs that are not fully transparent.22 In May 2019, the agency granted an exemption from the 1940 Act to Precidian Investments’ nontransparent ETF structure, ActiveShares. The Precidian structure adds a new participant, the authorized participant representative (APR), to the creation and redemption process.23,24 The ETF sponsor hires the APR, which contracts with the AP to trade the basket of securities on its behalf. The sponsor also hires a trusted agent to provide real-time pricing data every second to the consolidated tape that exchanges use to report trades and quotes. Precidian worked with State Street and other ETF providers to develop the ActiveShares model.

In December 2019, the SEC approved exemptive relief for Blue Tractor Group’s Shielded Alpha ETF wrapper, which allows actively managed portfolio strategies to operate within an ETF structure without the risk of front-running or free-riding. The Shielded Alpha wrapper uses “proprietary math to generate daily a creation basket” while ensuring that “an advisor’s alpha generation and portfolio trading execution remain fully opaque,” according to Blue Tractor.25 The company insists that a Shielded Alpha wrapper is highly transparent and will promote “highly efficient primary and secondary market pricing and trading.”

Structures such as ActiveShares and Shielded Alpha — as well as systems employed by Fidelity Investments, Natixis Investment Managers and T. Rowe Price that use proxy portfolios in creation and redemption baskets — enable firms to construct actively managed funds that protect managers’ intellectual property while retaining such ETF benefits as tax efficiency and tradability in secondary markets using real-time pricing data.

At the same time, the use of artificial intelligence and machine learning is helping to launch a new class of exchange-traded products. Smart beta initiatives have expanded beyond the basic factors they first covered, and more exotic bond ETFs are being launched. Some of these exotic ETFs are very different from normal index-tracking funds: the FLAG–Forensic Accounting Long–Short ETF (which looks for accounting red flags), the AlphaClone Alternative Alpha ETF (which tracks U.S. equities with large exposure among top-performing hedge funds, based on publicly disclosed positions), Credit Suisse X-Links Gold Shares Covered Call ETN (which invests in the SPDR Gold Shares ETF, which trades under the symbol GLD, a physical gold ETF and one-month call options on GLD) and the Invesco S&P Spin-Off ETF (which tracks an index of U.S. equities that have spun off from their parent companies).

Risks as ETFs Get More Exotic

Many notable exotic ETFs that at one time garnered substantial assets no longer exist, including the Credit Suisse X-Links Merger Arbitrage Liquid Index ETN (which ceased trading in June 2016), the UBS ETRACS Daily Long–Short VIX ETN (which closed in August 2016) and the U.S. Equity High Volatility Put Write Index Fund (which was liquidated in June 2017). Of course, many normal ETFs also ceased to exist during the past decade, due to a shortage of invested assets or other issues. Of the 530 ETFs trading on U.S. exchanges in 2009, only 380 remain today.

Liquidity risk is an issue for ETFs of all shapes and sizes. The secondary markets where ETFs are bought and sold typically use the average volume of shares traded as a liquidity indicator. ETF creation and redemption in the primary market can affect this liquidity by changing the shares outstanding in the secondary market. The ease of creation and redemption by the APs depends on the liquidity of the underlying instruments. Therefore, the ETF shares’ liquidity in the secondary market is indirectly dependent on the liquidity of the underlying instruments — and less so on the dollar volume of the ETF shares traded.

At any time, a fraction of registered APs will be actively participating in the arbitrage process to keep ETF premiums or discounts to a minimum. If all the APs were to step away from an ETF for a short period, that ETF could act like a closed-end fund and trade at a premium or discount to the NAV. A case in point is the “flash crash” on Monday, August 24, 2015. That morning, the S&P 500 index dropped 5 percent within a few minutes of starting trading, at the same time that many NYSE stocks had a delayed opening because of a lack of bids, making it impossible for APs to establish the fair value of ETFs. Some major U.S. ETFs experienced a 50 percent deviation from NAV as many market makers stepped away from the ETF arbitrage process to minimize risk in what seemed like an irrational period in the market.26,27 High frequency trading orders exacerbated the situation and contributed to some of the strong short-term downward momentum. Stop-loss market orders from investors also kicked in, helping to prolong and intensify the crash.

Although ETFs did not cause the flash crash, some structural issues in their reopening mechanism affected their response to it. Reopening procedures were not coordinated among exchanges, resulting in different halting prices and periods at different exchanges. When trading in many of their underlying stocks halted, ETFs could not find NAVs that reflected the fair value of their holdings.

Regulators around the world are increasingly concerned that a rapid increase in market stress or a wave of selling could cause a breakdown on the market-making side of ETFs.28 After all, APs are not legally obligated to perform market making, and in a high-stress environment they could step away or liquidate ETF units at deep discounts. If liquidity of the underlying assets were to suddenly dry up, this risk could be priced into ETF quotes. To deal with this danger, ETFs track liquidity of their assets in addition to performance, especially in less liquid fixed income markets.

At the same time, the ETF market has grown to trillions of dollars in assets during a period of relative calm and has been tested only a few times by a high level of sustained market volatility. During the March 2020 market sell-off, some prominent corporate bond ETFs were trading at a 5 percent discount to NAV before the Federal Reserve offered assurances that it would include corporate bond ETFs in its liquidity operations.

Systemic risk could rise as a result of the popular practice among money managers of using bond ETFs as cash substitutes. During a market sell-off, it is not clear how easily these ETFs could be converted to cash. When fixed income money managers face client withdrawals from their non-ETF products, they might be forced to redeem distressed ETF shares for cash conversion. In such situations, price decoupling due to liquidity spread could put pressure on these institutions, increasing the risk of a broad contagion effect.

Conclusion

ETFs have exhibited tremendous growth over the past decade, most of it fueled by passively managed liquid products. The ETF market received an additional boost from recent changes in the U.S. regulatory environment that reduced barriers to entry and improved competition. And while both institutional and retail investors may use these exotic ETFs to fill gaps in their asset allocation and get around constraints, it is imperative that they fully understand the mechanics and risks underlying the particular ETFs they are trading.

Michael Kozlov is a Senior Executive Research Director at WorldQuant and has a PhD in theoretical particle physics from Tel Aviv University.

Ashish Kulkarni is a Vice President, Research, at WorldQuant and has a master’s in information systems from MIT and an MS in molecular dynamics from Penn State University.

Rohan Joshi is a Regional Research Director at WorldQuant and has a postgraduate diploma in management from the Indian Institute of Management, Ahmedabad.

Xin Li is a Vice President, Research, at WorldQuant and has a master’s in computer science from Tsinghua University.

Sopio Bitsadze is an Intern at WorldQuant as part of the IFC–Milken Institute Capital Markets Program and has a master’s in economics from Tbilisi State University.

Endnotes

- Stoyan Bojinov. “Why Are ETFs So Much Cheaper Than Mutual Funds?” ETFdb.com, June 24, 2015.

- Igor Tulchinsky et al. Finding Alphas: A Quantitative Approach to Building Trading Strategies. 2nd Cornwall, U.K.: John Wiley & Sons, 2020.

- “Largest ETFs: Top 100 ETFs by Assets.” ETFdb.com.

- James Lord. “BMO Forecasts ETF Assets to Grow to $10 Trillion by 2023.” ETFstrategy.com, Jan 31, 2018.

- Frances Denmark. “Happy 20th Birthday, ETFs: A Look Back at Nate Most and His Novel Idea.” institutionalinvestor.com, July 3, 2013.

- Kathleen Pender. “Nathan Most, Creator of Exchange-Traded Funds, Still a Visionary/He Foresees ETFs Rivaling, Even Replacing, Today’s Mutual Funds.” SFGate.com. July 18, 2000.

- Fred Jheon. “Structure of ETFs: Differences Between First-, Second-, and Third-Generation ETFs.” Exchange Traded Funds, Fall 2009; Volume 2009, Issue 1: 126–131.

- Securities and Exchange Commission Investor Bulletin: Exchange Traded Funds (ETFs), August 2012.

- “Index Replication: Principles and Applications.” DSC Quantitative Group, August 12, 2015.

- George Tsalikis and Simeon Papadopoulos. “ETFS — Performance, Tracking Errors and Their Determinants in Europe and the USA.” Risk Governance & Control: Financial Markets & Institutions 9, no. 4 (2019).

- Michael Grill, Claudia Lambert, Philipp Marquardt, Gibran Watfe and Christian Weistroffer. “Counterparty and Liquidity Risks in Exchange-Traded Funds.” European Central Bank Financial Stability Review, November 2018.

- Tsalikis and Papadopoulos.

- Grill, Lambert, Marquardt, Watfe and Weistroffer.

- Ibid.

- Rob Wherry. “Bear Stearns’s Good News: An ETF First.” Wall Street Journal, March 26, 2008.

- “Active Management ETF Overview.” ETF.com.

- Securities and Exchange Commission Release Nos. 33-10695: Exchange Traded Funds.

- Lizzy Gurdus. “American Century Launches First Actively Managed Hidden-Asset ETFs — Here’s What You Need to Know.” CNBC.com, April 9, 2020.

- “SEC Adopts New Rule to Modernize Regulation of Exchange-Traded Funds.” U.S. Securities and Exchange Commission, September 26, 2019.

- Ibid.

- Ibid.

- Rachel Evans. “ETFs That Hide Their Portfolios Get Go-Ahead From U.S. Regulator.” Bloomberg News, December 10, 2019.

- “Precidian Investments Receives Exemptive Relief from the SEC for Its ActiveShares® Intellectual Property.” PRNewswire, May 2019.

- “A New Milestone for Exchange Traded Funds.” State Street Corp., 2020.

- “The U.S. Securities and Exchange Commission Approves Exemptive Relief to Permit Blue Tractor Group’s Shielded Alpha℠ ETF Structure.” Globe Newswire, December 11, 2019.

- “Equity Market Volatility on August 24, 2015.” U.S. Securities and Exchange Commission, December 2015.

- Austin Gerig and Keegan Murphy. “The Determinants of ETF Trading Pauses on August 24th, 2015.” U.S. Securities and Exchange Commission, February 2016.

- Marco Pagano, Antonio Sánchez Serrano and Josef Zechner. “Can ETFs Contribute to Systemic Risk?” Advisory Scientific Committee, European Systemic Risk Board, June 2019.

Disclaimer

Thought Leadership articles are prepared by and are the property of WorldQuant, LLC, and are being made available for informational and educational purposes only. This article is not intended to relate to any specific investment strategy or product, nor does this article constitute investment advice or convey an offer to sell, or the solicitation of an offer to buy, any securities or other financial products. In addition, the information contained in any article is not intended to provide, and should not be relied upon for, investment, accounting, legal or tax advice. WorldQuant makes no warranties or representations, express or implied, regarding the accuracy or adequacy of any information, and you accept all risks in relying on such information. The views expressed herein are solely those of WorldQuant as of the date of this article and are subject to change without notice. No assurances can be given that any aims, assumptions, expectations and/or goals described in this article will be realized or that the activities described in the article did or will continue at all or in the same manner as they were conducted during the period covered by this article. WorldQuant does not undertake to advise you of any changes in the views expressed herein. WorldQuant and its affiliates are involved in a wide range of securities trading and investment activities, and may have a significant financial interest in one or more securities or financial products discussed in the articles.